The Rule of 72: How Fast Will Your Money Double?

A simple mental math shortcut to estimate investment growth, debt accumulation, and the impact of inflation in seconds.

Published on

Compound interest is powerful, but the math behind it can be complicated. What if you could calculate exactly when your investment will double in value—in your head, in just a few seconds?

Enter the Rule of 72. It is a classic mental math shortcut used by investors to estimate the impact of compound interest. Whether you are looking at stock market returns, savings accounts, or even the damaging effects of inflation, this simple rule gives you a surprisingly accurate timeline without needing a spreadsheet.

According to the U.S. Securities and Exchange Commission (SEC), understanding these concepts is critical for gauging whether your current savings plan will meet your long-term goals.

How the Formula Works

The formula is deceptively simple: You take the number 72 and divide it by your annual interest rate. The result is the approximate number of years it will take for your money to double.

72 ÷ Interest Rate = Years to Double

Real-World Examples

Let's look at two scenarios to see the difference a few percentage points can make.

Example 1: The High-Yield Savings Account

Imagine you have $10,000 in a savings account earning a 4% annual interest rate.

Math: 72 ÷ 4 = 18

Result: It will take approximately 18 years for your $10,000 to turn into $20,000.

Example 2: The Stock Market Portfolio

Now, assume you invest that same $10,000 in a diversified portfolio with an expected average return of 8%.

Math: 72 ÷ 8 = 9

Result: It will take just 9 years to double your money.

By doubling the interest rate, you cut the waiting time in half. This highlights why finding competitive returns is crucial for long-term wealth building.

Visualizing the acceleration of wealth: Higher rates drastically reduce the time to double.

The "Reverse" Rule: Inflation and Debt

The Rule of 72 isn't just for happy investment returns; it also works for things working against you.

Inflation: If inflation averages 3%, dividing 72 by 3 gives you 24. This means the purchasing power of your cash will be cut in half in 24 years.

Credit Card Debt: If you have credit card debt at 18% interest, 72 divided by 18 is 4. Without payments, your debt balance would effectively double in just 4 years.

The Math Behind the Magic (Why 72?)

For the curious, the Rule of 72 is derived from the natural logarithm of 2. In mathematics, ln(2) is approximately 0.693, a concept detailed in courses at institutions like Stanford University.

If we were being perfectly precise, we would use the "Rule of 69.3". However, dividing by 69.3 is difficult to do in your head. The number 72 is chosen because it is close to 69.3 and has many convenient divisors (2, 3, 4, 6, 8, 9, 12). This makes it the perfect compromise for simplicity.

Need Exact Numbers?

While the Rule of 72 is great for estimation, real financial planning requires precision. Use our free Compound Interest Calculator to see exactly how your money grows over time.

Is it precise?

The Rule of 72 is most accurate, again, as an estimation, for interest rates between 6% and 10%.

- For very low rates: The rule slightly overestimates the time.

- For very high rates: The rule slightly underestimates the time.

However, for a quick "back of the napkin" calculation, it remains the industry standard used by financial advisors and institutions worldwide.

| Method | What you do | Best use |

|---|---|---|

| Rule of 72 | Divide 72 by the annual rate expressed in percent (for example 8% → about 9 years to double). | Mental math in meetings, podcasts, or quick sanity checks on compound growth or debt. |

| Exact logarithmic math (ln) | Use ln(2)/ln(1+r) with r as a decimal for precise doubling time under standard discrete (annual) compounding. | Spreadsheets, planners, or anytime you are locking a contractual or legal number. |

| Rule of 69.3 | Divide 69.3 by the percent rate—closer to the continuous ideal but harder to do mentally. | Teaching why 72 is a deliberate compromise between accuracy and divisibility. |

Beyond Doubling: The Rules of 114 and 144

If you want to look even further into the future, you don't have to stop at doubling. There are two "cousin" rules that help you calculate how long it takes to triple or quadruple your money using the same mental math logic.

- The Rule of 114 (Tripling): Divide 114 by your interest rate to see how long it takes to triple your investment. At a 10% return, your money triples in about 11.4 years.

- The Rule of 144 (Quadrupling): Divide 144 by your interest rate to see how long it takes to quadruple your investment. At that same 10% return, your money quadruples in 14.4 years.

Three rules, one rate (example: 10% per year)

Illustration only—swap 10% for your own rate; the pattern (divide 72, 114, or 144 by that rate) stays the same.

Notice the relationship: 144 is exactly double 72. This confirms the mathematical consistency of compounding—it takes the same amount of time to go from $100 to $200 as it does to go from $200 to $400.

The "Tax Drag" Adjustment

A critical variable in any compound interest calculation is the distinction between your 'Gross' interest rate and your actual 'After-Tax' return. If your money is in a taxable account, the government is going to take a cut of your gains every year. This is known as "Tax Drag," and it slows down your doubling time significantly.

To get a "Definitive" estimate, you should use your After-Tax Return. For example, if you earn 8% but are in a 25% tax bracket, your real growth rate is 6%.

Pro Math: 72 ÷ 6 = 12 years to double (instead of the 9 years you'd expect at 8%).

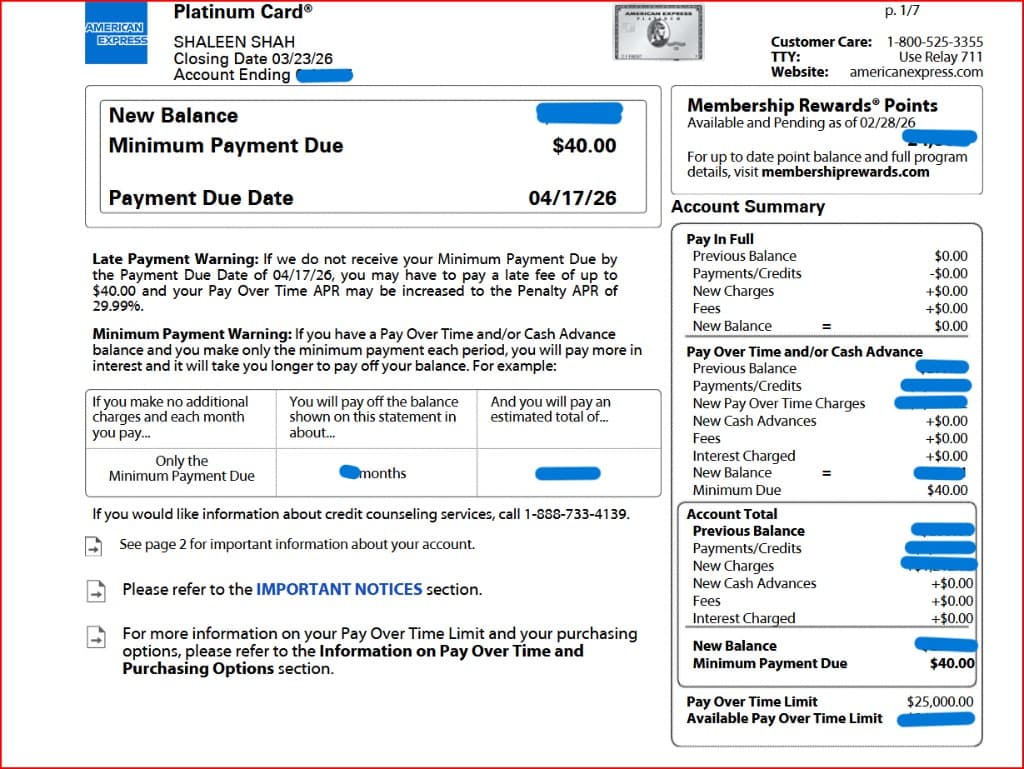

The "Rule of 76" for High-Interest Debt

While 72 is the "magic number" for standard investments (6%–10%), the math shifts when you deal with very high interest rates, like credit cards or predatory loans. As the interest rate climbs above 20%, the Rule of 72 starts to "underestimate" how fast the debt grows.

Swipe horizontally to view the full-width screenshot.

Real-World Evidence: An American Express Platinum statement summary. It is a common misconception that high APRs only apply to entry-level credit; as seen here, even premium products issued to those with strong credit standing carry rates that trigger aggressive compounding. When rates climb into this 20-30% range, the Rule of 72 underestimates the growth of debt, making the Rule of 76 the definitive math for protecting your wealth.

For high-interest calculations, experts often switch to the Rule of 76. If you have a credit card balance at 24% interest and you make no payments, your debt won't just double in 3 years (72 ÷ 24); the aggressive daily compounding means it will likely double even faster. Using 76 gives a more conservative and realistic warning of how quickly high-interest debt can spiral out of control.

Compounding "Invisible" Assets

The most unique way to use this math is applying it to your own skills and productivity. If you focus on getting just 1% better at a specific skill every week, how long until you are "twice as good"?

Using the Rule of 72, you can see that with 1% weekly improvement, your capability doubles in approximately 72 weeks (about 1.4 years). This illustrates the mathematical power of consistency. Whether it is money, health, or knowledge, compounding rewards those who stay the course.

Summary: Key Takeaways

- The Formula: Divide 72 by your annual interest rate to find the years required to double your capital.

- Works Both Ways: Use it to calculate investment growth, but also to calculate the speed of debt accumulation or inflation.

- Accuracy: It is most accurate for rates between 6% and 10%.

- Next Step: For precise planning, always run the numbers through a formal calculator.